The Fed's Balancing Act

- Betty Joyce Nash, Carolina Commentary

- Aug 14, 2024

- 3 min read

Raise your hand if you know what “the Fed” does, besides its responsibility for deciding the interest rates that ultimately affect our payments for mortgages, cars, credit cards, and more. Few know how the Fed operates, though everybody cares deeply about their pocketbooks. Among other chores, such as supervision and regulation, the Fed closely tracks the economy in order to make policy decisions. Its Congressional mandate? Maximum employment, stable prices, and moderate long-term interest rates.

In July, we the people figured there’d be a rate cut. We knew the Fed had begun raising rates against inflation in 2022, as spending roared back after the pandemic shutdown. Inflation refers to prices continuing to rise over time. This erodes purchasing power.

But no. Rates remain between 5.25 percent and 5.50 percent.

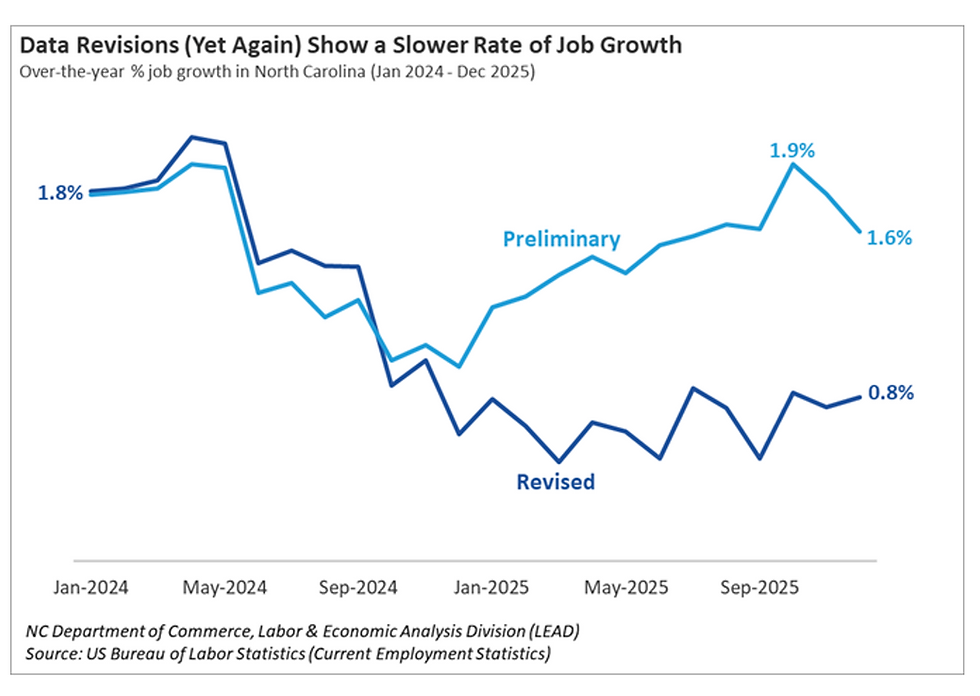

Included in the Fed’s rationale is a reference to “disappointing jobs data.” However, the chairman of the Fed’s Federal Open Market Committee [FOMC], Jerome Powell, said if labor markets strengthen, a September rate cut is likely. Business Insider reports that the July jobs report “came in cooler than expected, with the US economy adding 114,000 jobs. The unemployment rate rose to 4.3%.” This triggered a widely-respected rule—the Sahm-rule recession indicator, which has a perfect track record in identifying downturns in real time.

Maximum employment is defined as the greatest number of people employed, or fewest unemployed, that the economy can manage and still keep prices stable. The unemployment rate and prices work in tandem. The economy is dynamic, ever-changing. If most people have jobs, a firm would struggle to find workers. They would need to raise wages to attract employees. That cost would be passed along to customers in the form of higher prices.

Indeed that happened in North Carolina, post-pandemic, according to N.C. State’s economist Mike Walden, when the economy re-opened, and, with federal assistance still coming in, people sought different work.

“How did these industries react to the shortages? They reacted the way economists would expect. They made their jobs more attractive to workers, especially by increasing the pay. For example, in North Carolina between 2019 and 2024, average hourly wage rates rose three times faster in leisure/hospitality and construction, and two times faster in education/health care and general service jobs compared to the increase for the average job.” The wage increases also outpaced price increases (inflation) over the same time period. Walden adds that he expects the annual inflation rate to come very close to 2% by the end of 2024. “I wouldn’t be surprised to see the Fed reduce their benchmark interest rate by two percentage points in the second half of 2024.”

In setting rates, the FOMC depends on current international, and regional economic intelligence. Committee members assess economic conditions in light of the Congressional mandate of maximum employment and price stability. Price stability means a low and stable rate of inflation, ideally, 2 percent. That target is coming closer to reality.

The “FOMC” stands for Federal Open Market Committee, which consists of the seven members of the Federal Reserve Board of Governors who determine rates: the president of the Federal Reserve Bank of New York and four other regional Reserve Bank presidents, who serve one-year terms on the FOMC, on a rotating basis, with the other Reserve Bank presidents.

At FOMC meetings, the senior official at the Federal Reserve Bank of New York, for instance, discusses financial and foreign exchange markets, plus the New York Fed's Trading Desk, where U.S. government securities are bought and sold. Staff from regional reserve banks’ boards of governors discuss their districts’ economic and financial conditions and forecasts. The board of governors and all 12 Reserve Bank presidents—whether they’re voting members that year or not—assess recent developments in their districts and the overall economic outlook from which they determine the interest rate.

Betty Joyce Nash reported for the Greensboro News & Record and the Hendersonville Times-News before moving to Virginia where she worked as an economics writer for the Federal Reserve Bank of Richmond. She co-edited Lock & Load: Armed Fiction, an anthology of literary short stories that probe Americans' complicated relationship to firearms. (University of New Mexico Press, 2017.)

Comments